By Rupesh Kumar

Published: September 29, 2025

Last Updated: February 23, 2026

Introduction

I’ll be honest — for a long time, I struggled to save money every month. My salary was decent, but by the third week, my bank balance would almost touch zero. I kept wondering how my money disappeared so fast. This problem happened to me again and again. Then I decided to seriously learn how to save money from salary every month instead of just complaining. I started creating a simple monthly savings plan, testing different methods to find the best way to save money monthly. Slowly, I understood that learning how to save money every month is not about earning more — it’s about managing smarter.

I will guide you in this post step-by-step, just like I guided myself when I finally decided to take control of my money. I’ll share what worked for me, what mistakes I made, and what changes actually helped me save money every month consistently. No complicated finance terms, no unrealistic advice — just simple, practical steps that you can apply from your next salary itself.

Why It’s Important to Save Money Every Month

When I started to save money every month consistently, I noticed three big changes:

- I stopped stressing about emergencies.

- I felt more confident about my future.

- I stopped depending on credit cards.

Small monthly savings create big financial stability.

Life is unpredictable. Medical bills, sudden travel, job delays — anything can happen. If you build the habit to save money every month, you stay prepared.

How to Save Money Every Month – 10 Smart and Practical Tips

1. Track Every Rupee (or Dollar) You Spend

The biggest reason people fail at saving is they don’t know where their money goes. Small things like daily coffee, snacks, or online subscriptions may look harmless, but when added up, they eat a big part of your income.

Example:

Spending ₹100 ($1.20) on coffee daily = ₹3,000 ($36) a month. That’s ₹36,000 ($430+) a year.

💡 Tip:

Use apps like Walnut, Money View, Mint, or even a simple Google Sheet to track expenses. Review weekly to spot wasteful spending.

Try this tool →Use SmartKharch – Monthly Income & Expense Tracker (100% free, browser-based) to quickly record your income and expenses every month.

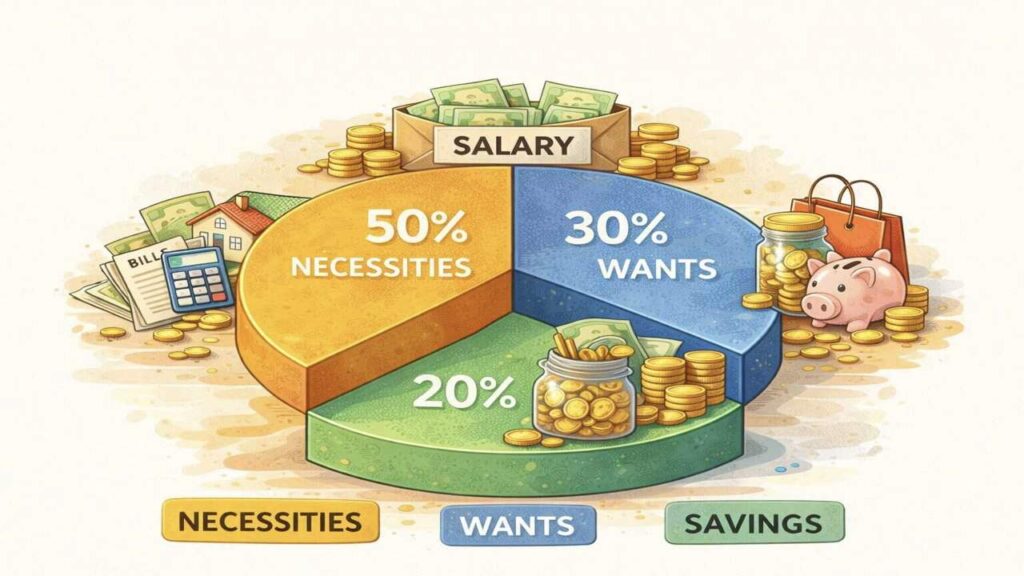

2. Create a 50/30/20 Budget Rule

Budgeting doesn’t have to be boring. The 50/30/20 rule is simple and flexible. The 50/30/20 rule is a globally popular budgeting method. I follow the 50/30/20 rule, which is a globally accepted budgeting framework explained in detail on Investopedia.

- 50% Needs → Rent, groceries, bills, transport

- 30% Wants → Shopping, Netflix, dining out

- 20% Savings/Investments → Emergency fund, SIPs, retirement

Example:

If you earn ₹50,000/month, allocate ₹25,000 to needs, ₹15,000 to wants, and ₹10,000 to savings.

💡Tip: Automate the 20% savings so you don’t get tempted to spend it.

3. Cook More, Order Less

Food delivery is convenient but costly. Cooking at home saves money and is healthier too.

Example:

Ordering dinner online costs ₹500, but cooking the same meal at home may cost just ₹150. Do this thrice a week, and you save over ₹4,000/month.

💡 Tip: Plan your weekly meals and prep in advance. Keep quick recipes ready for busy days.

4. Cancel Unused Subscriptions

Streaming platforms, gym memberships, and premium apps quietly drain your wallet. Many people forget they are even paying for them.

Example:

Netflix + Spotify + Amazon Prime = ₹1,500/month. If you only use one, cancel the rest and save ₹1,000/month.

💡 Tip: Review bank statements monthly to spot unused subscriptions and cancel immediately.

5. Switch to Digital Payments with Rewards

UPI apps, credit cards, and digital wallets often give cashback, reward points, or discounts. Smart usage helps you save on routine expenses.

Example:

Paying your electricity bill via Google Pay can give ₹50 cashback. Over a year, such rewards can add up to thousands.

💡 Tip: Use rewards only on things you genuinely need, not just to “claim cashback.”

⚠️ Caution: Pay credit card bills in full every month to avoid high-interest charges.

6. Buy in Bulk (But Smartly)

Buying in bulk reduces the per-unit cost of essentials like rice, flour, or cleaning products. But overstocking leads to waste.

Example:

A 5 kg rice pack may cost ₹450, while 1 kg packs cost ₹110 each. Bulk purchase saves ₹100 right away.

💡 Tip: Buy bulk only for items you consume regularly and that have a long shelf life.

7. Choose Generic Brands Over Premium

Branded items are often overpriced due to advertising. Generic or store brands usually offer the same quality at a lower price.

Example:

Generic paracetamol may cost ₹10, while a branded version costs ₹25. Same medicine, higher price.

💡 Tip: For groceries, cleaning supplies, and medicines, test generic brands—you’ll hardly notice the difference except in price.

8. Limit Impulse Shopping

Impulse buying is one of the fastest ways to lose money. Sales and flashy ads tempt us, but most purchases are not truly needed.

Example:

Buying a “deal of the day” gadget for ₹2,000 that you never use is just wasted money.

💡 Tip: Follow the 24-hour rule—if you still want it after a day, then buy. Often, the urge disappears.

9. Automate Your Savings

Instead of saving “whatever is left” at month-end, make savings automatic. Set up auto-debit to transfer money into a savings or investment account right after your salary arrives.

Example:

Auto-transferring ₹5,000 monthly into a recurring deposit = ₹60,000 saved in a year, without effort.

💡 Tip: Treat savings like a non-negotiable bill. Pay yourself first.

10. Invest Instead of Just Saving

Saving is important, but money sitting idle loses value because of inflation. Investments grow your wealth over time.

Example:

Investing ₹2,000/month in a SIP with 12% annual returns = ₹4.7 lakh in 10 years.

💡 Tip: Start small with safe options like SIPs, PPF, or index funds. Gradually explore stocks or ETFs as you learn more.

How Much Money Should You Save Every Month ?

There is no fixed number.

Start with:

- Even 5–10% of income

- Increase gradually

- Focus on consistency

Saving regularly matters more than saving big amounts.

Real Personal Example

In 2022, I used to live paycheck-to-paycheck. My salary was ₹45,000, but by the 20th, my balance would be under ₹1,000. I didn’t realize where it all went — until one day I tracked every expense for a month.

Here’s what I found:

- Food delivery: ₹3,800

- Shopping: ₹2,600

- Travel (Uber, autos): ₹1,500

- Subscriptions: ₹1,200

That’s ₹9,100 gone every month on things I could control.

The next month, I made three small changes — cooking more, cancelling unused subscriptions, and setting up auto-savings. Within three months, I managed to save ₹10,000 monthly.

By 2026, my income increased to ₹60,000 — but my savings increased faster. Today, I easily save ₹15,000–₹18,000 a month without cutting out enjoyment.

Common Mistakes People Make

No Clear Plan: I used to save “whatever was left.” That never worked. You must plan savings before spending.

Impulse Shopping: I’d buy things just because there was a “Sale.” Discounts made me spend more, not less.

Ignoring Small Expenses: Coffee, snacks, cabs — tiny amounts pile up fast.

Using Credit Cards Wrongly: I’d pay the minimum balance and keep adding more. Interest charges killed my savings.

Comparing with Others: Trying to keep up with friends’ lifestyles made me overspend.

Once I accepted these mistakes, saving became much easier and natural.

Limitations & Disclaimer

This content is only for general information on how to save money every month. It is not financial advice. Your savings depend on your income, expenses, lifestyle, and habits. Results can be different for each person.

Before making any financial decision, check your own budget and needs. We are not responsible for any loss or money problems. Always plan your spending carefully and save as per your situation.

Frequently Asked Questions

Q1. How can I save money every month on a low salary?

Start by tracking every expense for one month. I noticed that small daily spending was my biggest problem. Cut 2–3 unnecessary expenses and save at least 10% of your income first. Even ₹500–₹1,000 monthly is a good start.

Q2. What is the best way to save money monthly?

The best way to save money monthly is to automate your savings on salary day. Transfer money to a separate account before you start spending. When I did this, saving became automatic and stress-free.

Q3. Why do I fail to save money every month?

Most people fail because they save after spending. This problem happened to me too. The solution is simple — save first, spend later. Also avoid impulse shopping and unnecessary subscriptions.

Q4. Is the 50/30/20 rule good for beginners?

Yes, it is simple and practical. It gives clear limits for spending and saving. I found it very easy to follow compared to complicated budgeting methods.

Q5. Can I enjoy life and still save money every month?

Absolutely. Saving does not mean cutting all fun. It means planning smartly. I still travel and enjoy outings, but I budget them properly. Balance is the key.

Conclusion

Saving money every month is not about being rich or earning a huge salary. I learned this the hard way. When I started focusing on small habits instead of big promises, everything changed. I noticed that controlling just a few unnecessary expenses made a big difference in my savings.

If you truly want to save money every month, don’t wait for the “perfect time” or a salary increase. Start with what you have today. Create a simple monthly savings plan, automate your savings, and stay consistent. Some months will be better, some will be tight — and that’s completely normal.

From my own experience, financial peace doesn’t come from earning more. It comes from managing wisely. Start small, stay disciplined, and trust the process. One day, you’ll look at your savings and feel proud that you began.

You can also read this

How to Manage Daily Expenses and Save Money – 10 Easy Tips