By Rupesh Kumar

Published: September 26, 2025

Last Updated: February 19, 2026

Introduction

I still remember the day my credit card application was rejected. I had a stable job, regular income, and no major financial problems. Still, the bank said my credit score was too low. That moment was confusing and honestly a little embarrassing. I had never paid serious attention to my credit profile before.

In India, we often focus on saving money, investing in SIPs, buying gold, or planning EMIs. But very few people understand how important a credit score is. I realised its value only when I applied for a car loan and was offered a higher interest rate than my colleague. The difference was simple — his score was above 780, and mine was just 642.

That experience pushed me to learn how to improve credit card score properly. I did not look for shortcuts. I focused on small habits and consistent discipline. Over the next few months, I slowly rebuilt my credit profile and saw real improvement.

In this article, I will share the exact steps that worked for me — practical, realistic, and suitable for Indian financial situations.

💳 What is a Credit Card Score ?

A credit card score, commonly known as a CIBIL score, is a three-digit number between 300 and 900 that shows how well you manage credit. Banks check this number before approving loans or new credit cards. It is based on your payment history, credit usage, loan behaviour, and overall financial discipline.

If you regularly pay your bills on time and keep your card usage low, it helps improve credit card score steadily. Many people search for how to improve CIBIL score or how to improve credit score fast, but the real answer is simple — consistent and responsible usage.

If you are just starting and wondering how to build my credit, begin with small transactions and pay them fully on time. Over a few months, these habits help increase credit score quickly in a safe and practical way.

Why You Should Improve Credit Card Score

Improving your score is not just about loans. It affects many financial areas.

Fast Loan Approval: After my score crossed 750, loan approval became smooth. Fewer verification calls. Less stress.

Lower Interest Rates: Even a 1% lower interest rate on a home loan can save lakhs over time.

Higher Credit Limits: Credit card companies offer better limits and benefits when your score improves.

Financial Reputation: In India, your credit score reflects your financial discipline. A good score means trust.

Emergency Support: In urgent situations, banks trust people with good credit history.

10 Powerful Ways to Improve Credit Card Score Fast

These are not theory-based tips. These are habits I personally followed.

1. Always Pay Your Bills on Time

This is the most important habit for improving your credit score fast. Even one late payment can pull your score down sharply. I once missed a due date during a festival and saw my score drop by 40 points. Set reminders or use auto-pay — timely payments show lenders you’re responsible and trustworthy.

👉 Paying on time is the fastest way to improve credit card score and build long-term credit reliability.

2. Pay Full Amount, Not Just Minimum Due

I used to think paying the minimum due was enough to stay safe — but that’s a big mistake. The remaining balance keeps adding heavy interest and hurts your credit score. Now, I always pay the full bill amount every month, even if it means cutting a few extra expenses. It keeps my score strong and debt under control.

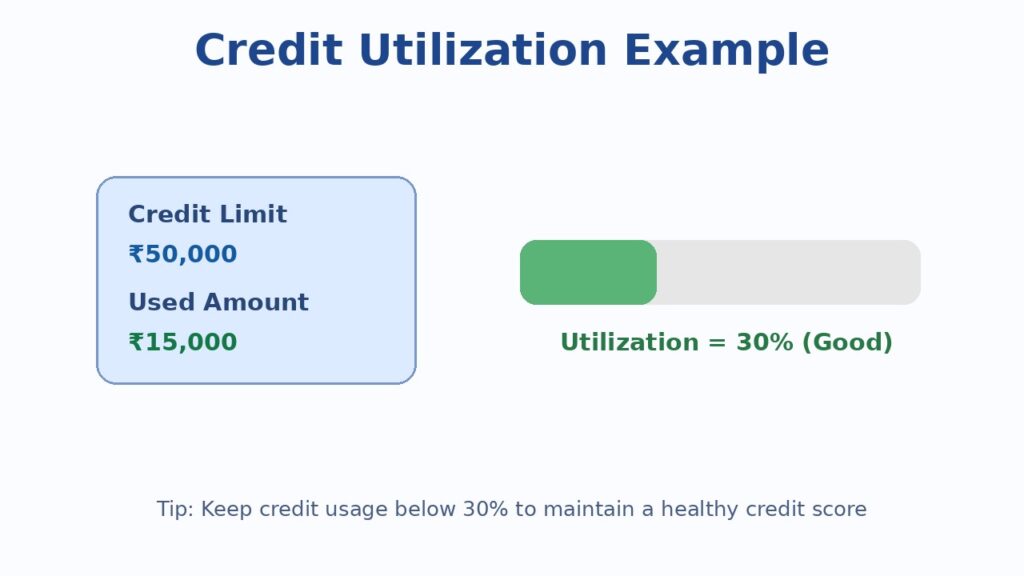

3. Keep Credit Utilization Below 30%

This step made a huge difference for me.

If your limit is ₹1,00,000, try not to use more than ₹30,000 regularly.

People often search how to increase credit score quickly, but they ignore this basic rule. High usage signals risk to banks.

4. Use a Secured Credit Card If Needed

If your score is very low, normal cards may get rejected.

In such cases, a secured credit card against a fixed deposit is helpful.

This is a practical answer for people asking how to build my credit from scratch.

5. Request a Credit Limit Increase

After maintaining good payment history for a year, I requested a credit limit increase on my main card. It didn’t mean I started spending more — it just lowered my credit utilization ratio. This small change boosted my score within weeks. Higher limits used wisely show banks that you can handle credit responsibly and smartly.

6. Clear Small Dues First

When I decided to fix my financial habits, I cleared smaller pending amounts first.

It reduced my outstanding balance quickly and improved my overall profile.

If you’re thinking about how to increase credit score quickly, start by clearing all pending dues.

7. Avoid Too Many Loan or Card Applications

When you apply for multiple cards or loans, each lender checks your report.

Too many checks lower your score slightly.

If you are serious about how to improve CIBIL score, avoid unnecessary applications.

8. Check Your Credit Report Regularly

I ignored my credit report for years, thinking it didn’t matter — until I found an error that cost me 25 points. Now, I check it every few months for wrong entries or old dues. You can download it free from CIBIL or Experian once a year. Keeping an eye on your report helps you fix issues before they hurt your score.

9. Maintain Old Credit Cards

I once made the mistake of closing my oldest credit card, thinking I was simplifying my finances. But that old card carried years of good history, and my score dropped soon after. Now, I keep my oldest card active by using it for small monthly expenses. Longer credit history always strengthens your credit score and builds trust with lenders.

10. Stay Consistent and Patient

There are no overnight tricks.

Many people search how to improve credit score fast expecting instant results. In reality, steady discipline works better than shortcuts.

Within six to eight months of consistent effort, I saw major improvement.

Real Personal Example

A few years ago, I had two credit cards and one personal loan. Life got hectic, and I missed a couple of payments. I didn’t realise how badly that affected my credit score until I applied for a home loan — and got rejected. My score was just 642.

Instead of panicking, I made a plan. I started paying every bill on time, reduced my spending to 30% of my limit, and cleared small pending dues first. I also checked my credit report and found one error that I immediately corrected.

Within six months, my score improved to 710. By the end of the year, it reached 780. I finally got my home loan approved easily — and with a lower interest rate. That moment made every small effort worth it.

Common Mistakes People Make

I’ve made most of these mistakes myself — and I’ve seen friends struggle because of them too. If you genuinely want to improve credit card score, avoiding these common errors is just as important as following good habits.

Missing Payment Dates: Even a one-day delay can hurt your score. I learned this after forgetting a bill once during Diwali week.

Paying Only the Minimum Amount: I used to think paying the minimum due was fine — it wasn’t. It kept increasing my interest.

Using Too Much Credit: If your card limit is ₹1,00,000 and you regularly spend ₹90,000, banks see you as credit-dependent. High utilisation makes it harder to increase credit score quickly. Try to stay below 30% usage.

Too Many Loan Applications: Every time you apply for a loan or card, your score takes a small hit.

Closing Old Cards: Old cards build history. I once closed one and lost valuable credit age.

Ignoring Credit Report Errors: Once, a wrong entry in my CIBIL report kept my score low for months until I got it corrected.

Avoiding these simple mistakes can save you months of frustration and make your journey toward a strong credit profile much smoother.

Limitations & Disclaimer

This content is only for general information to help you understand how to improve credit card score. It is not financial advice. Your credit score depends on many factors like payment history, credit usage, income, and bank policies. Results may be different for each person.

Before taking any financial decision, please check with your bank or a financial expert. We are not responsible for any loss or issue based on this information. Always use credit cards carefully and spend within your limit.

Frequently Asked Questions

1. How to improve CIBIL score after late payment?

Clear the overdue amount immediately and maintain perfect payment history for the next few months.

2. How to increase credit score quickly?

There is no magic shortcut. Reduce credit usage, avoid new loans, and pay bills on time.

3. Does checking my own score reduce it?

No. Checking your own score is a “soft inquiry” and doesn’t affect your rating.

4. How to build my credit if I have no history?

Start with a secured credit card or small loan and repay responsibly.

5. Should I take a new loan to improve my credit mix?

Only if you truly need it. Don’t take loans just for the sake of improving your score.

6. Can I fix errors in my CIBIL report ?

Yes. Contact the credit bureau and the lender to correct wrong entries. It usually takes a few weeks.

Conclusion

Improving your financial profile is not about shortcuts. It is about discipline and consistency. If you truly want to improve credit card score, focus on paying on time, reducing credit usage, and avoiding unnecessary loan applications. Many people search for how to improve CIBIL score or how to improve credit score fast, but the real answer lies in simple daily habits. If you are starting fresh and wondering how to build my credit, begin small and stay patient. Over time, these smart decisions will naturally help you increase credit score quickly and build long-term financial trust.