By Rupesh Kumar

Published: September 22, 2025

Last Updated: February 18, 2026

Introduction

I still remember when I received my first salary. I felt proud and started saving money in my bank account every month. For some time, I believed saving alone was enough. But slowly I noticed something — my money was not growing, while daily expenses were increasing. That’s when I started learning about the best investment options in India.

In the beginning, understanding different investment options in India was confusing. There were many choices like Fixed Deposit, PPF, mutual funds, gold, and stocks. My parents suggested safe investment options in India, while my friends talked about SIPs and market returns.

So I started small and explored investment options in India for beginners. Over time, I realised the best investment options in India are not about quick profit — they are about consistency and patience.

Why Investing Is Necessary

Living costs are increasing every year. Expenses like education, healthcare, travel, and retirement planning require proper financial planning.

If money stays in a savings account, it grows very slowly. But when you invest wisely, your money can grow over time and help you achieve financial goals.

Benefits of investing:

Beat inflation: Savings accounts usually give around 3–4% interest, while inflation averages 6–7%.

Grow wealth over time: Long-term investments can multiply your savings through compounding.

Achieve financial goals: Buying a house, retirement planning, children’s education, or starting a business all require planned investments.

Financial security: Investments create stability and reduce dependency on one income source.

One thing I learned personally — consistency matters more than amount. Even small investments grow significantly over time.

How to Choose the Best Investment Options in India

Before selecting from the many investment options in India, understanding your situation is important.

1. Risk Tolerance

- Low risk: Capital protection is priority

- Medium risk: Balanced growth with safety

- High risk: Higher return potential with volatility

When I started investing, I realised I was a medium-risk investor. That clarity helped me choose better options.

2. Investment Horizon

- Short term: Less than 3 years

- Medium term: 3–7 years

- Long term: 7+ years

Longer duration usually allows safer recovery from market fluctuations.

3. Financial Goals

Investments should match goals like:

- Emergency fund

- Home purchase

- Wealth creation

- Retirement planning

- Child education or marriage

Without a goal, investing becomes random.

Once you understand these, selecting investment options in India becomes easier.

Top 10 Best Investment Options in India for Safe and High Returns

Let’s look at the most practical and widely used investment options in India today.

1. Fixed Deposit (FD)

For most Indian families, Fixed Deposits are the first step toward investing. My parents still prefer FDs over anything else. And honestly, they’re not wrong — FDs are reliable and easy to manage.

Key Features

- Fixed returns (around 6–8%)

- Low risk

- Suitable for short to medium term

Pros

✔ Capital safety

✔ Predictable returns

Cons

✘ Returns may not beat inflation

✘ Interest is taxable

FD is suitable for people who want security and guaranteed returns.

2. Public Provident Fund (PPF)

PPF is a government-backed scheme that’s perfect for long-term savings. My father opened one for me when I started my first job — I didn’t realise how useful it would be.

Why it’s great

- Lock-in period: 15 years

- Tax-free returns

- Backed by the Government of India

Pros

✔ Safe and stable

✔ Excellent for long-term savings

Cons

✘ Long lock-in

✘ Limited annual contribution

For long-term investors, PPF is one of the best investment options in India.

3. Employees Provident Fund (EPF)

EPF is a retirement savings scheme mainly for salaried employees in India. Both the employee and employer contribute a fixed percentage of salary every month to the EPF account.

It is considered one of the safest long-term investment options because it is supported by the government and offers stable interest rates.

The biggest advantage of EPF is that it helps build a retirement fund automatically through regular contributions.

Why EPF Is Important

- Best for: Retirement savings

- Risk level: Low

EPF is especially useful for salaried people who want disciplined long-term savings without actively managing investments.

4. National Pension System (NPS)

The National Pension System (NPS) is a government-backed retirement investment scheme designed to help people build a pension fund for the future. It is available for both salaried and self-employed individuals in India.

In NPS, your money is invested in a mix of equity, corporate bonds, and government securities, which helps balance risk and returns over the long term.

Why it’s good

- Market-linked returns

- Low fund management cost

- Additional tax benefits

- Risk level: Low to medium

- Returns: Moderate to good (long-term)

Drawbacks

- Partial withdrawal restrictions

- Meant mainly for retirement

For long-term financial security, this can be part of the best investment plan in India.

5. Mutual Funds – Smart Growth for Modern Investors

Mutual Funds are no longer just for finance experts. With SIPs and mobile apps, anyone can start investing easily.

- Equity Funds :- High returns, high risk

- Debt Funds :- Lower returns, stable, safer

- Hybrid Funds :- Balance of both

- Risk :- Medium

- Best for: Long-term wealth creation

Why Invest ?

- Average equity MF returns :- 12%–18% annually (long-term)

- SIP option allows investment from ₹500/month

- Professional fund management

💡 Example :- A monthly SIP of ₹5,000 in an equity fund for 15 years can grow into ₹25–30 lakh depending on market performance.

Best for: Beginners who want high returns without choosing individual stocks.

6. Exchange Traded Funds (ETFs) – Low Fees, High Clarity

ETFs are similar to mutual funds but traded like stocks on the stock exchange. They usually have lower costs and track market indexes. They’re perfect if you already have a Demat account.

Advantages :-

- Low expense ratio compared to mutual funds

- High liquidity – Easy to buy/sell anytime during market hours

- Transparent portfolio

- Risk :- Medium

- Best For :- Beginners entering stock markets with low cost

ETF vs Mutual Fund: Which is Better for Beginners ?

ETFs are becoming modern investment options in India for long-term investors.

7. Real Estate – Long-Term and Tangible

Real estate remains a favorite in India for its dual benefits :- capital appreciation and rental income.

- Pros :- Tangible asset, steady income, hedge against inflation

- Pros :- Can generate passive income through rent

- Cons :- High initial investment

- Cons :- Less liquid compared to other options

- Risk :- Medium

- Best For :- Investors with capital for long-term holdings

For those with capital, real estate can still be part of the best investment plan in India.

8. Gold – Evergreen and Trusted

Gold has always been trusted in Indian households.

It helps diversify a portfolio and protect wealth.

Gold continues to be one of the traditional safe investment options in India.

Why it’s great

- Works as a hedge against inflation.

- Easily bought in digital form (SGBs or Gold ETFs).

- Liquidity — can sell quickly if needed.

- Best For :- Diversification and safety

Investing directly in stocks can generate high returns but comes with higher risk.

Beginners should start slowly and learn before investing large amounts.

Pros

✔ Potential returns 15–20%+ per year

✔ Ownership in companies ✔Dividends plus capital growth

Cons

✘ Requires knowledge and discipline

✘ Market volatility

Best for: Young investors ready to learn and take calculated risks.

Caution :- Requires good knowledge, patience, and risk tolerance.

For experienced investors, stocks are powerful investment options in India.

👉 To track live Nifty and Sensex data, visit the official NSE India website, which provides real-time market updates and investment insights.

Complete Share Market Guide for Beginners: How to Invest

10. Cryptocurrencies – Digital Assets

Crypto is still a high-risk, high-reward option in India. Though highly volatile, cryptocurrencies like Bitcoin and Ethereum are attracting young Indian investors.

- Pros :- Potential for very high returns

- Pros :- Global accessibility

- Cons :- Not fully regulated in India

- Cons :- Price volatility is extreme

- Risk :- Very High

- Best For :- High-risk takers

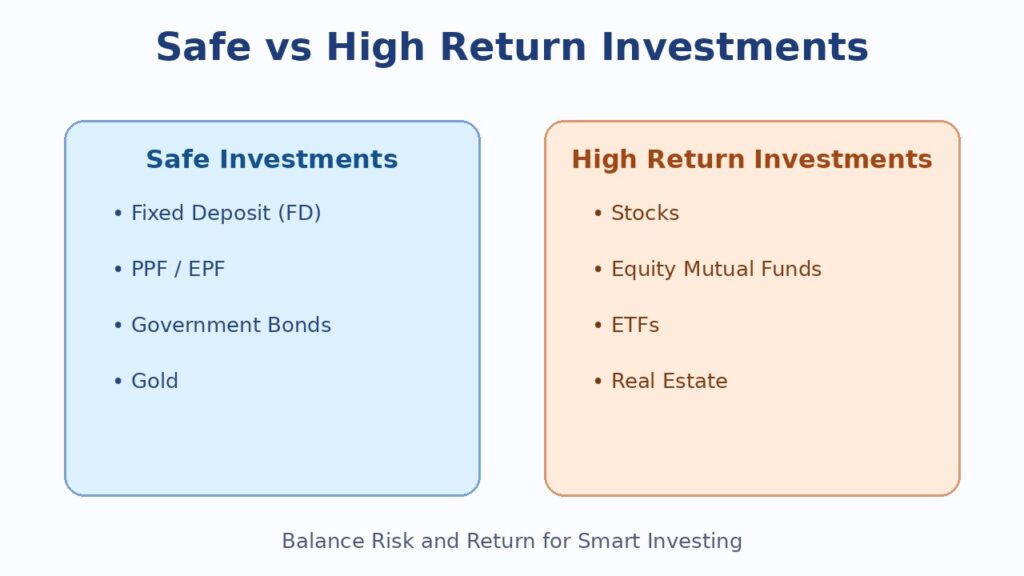

Best Investment Options by Risk Category

Low Risk

- FD

- PPF

- EPF

- Gold

- Post Office Schemes

Medium Risk

- Hybrid Mutual Funds

- NPS

- ETFs

High Risk

- Equity Mutual Funds

- Stocks

- Crypto

A balanced portfolio usually includes a mix of these best investment options in India.

Frequently Asked Questions

1. What is the safest investment in India right now?

PPF, FDs, and Government Bonds are safest — they offer stable returns with zero risk of loss.

2. Which investment gives the highest return in 2026 ?

Equity Mutual Funds and stocks can give the best long-term returns, but they also have higher risk.

3. Can I start with small monthly investments ?

Yes, SIPs in Mutual Funds start from ₹500, and even ETFs can be bought for ₹100. Small steps matter.

4. Is 2026 a good time to invest ?

Yes. India’s economy is strong, inflation is stable, and digital access has made investing easier than ever.

5. Which investment is best for beginners ?

Start with Mutual Funds (SIPs). They’re simple, balanced, and give good long-term growth.

6. How can I balance safety and high returns?

Follow the 60–40 rule — 60% in safe investments (PPF, FD, Bonds) and 40% in high-return options (Stocks, Mutual Funds, ETFs).

⚠️ Limitations & Disclaimer

This article is for educational and informational purposes only. It does not provide financial or investment advice. I am not a SEBI-registered financial advisor. Investment options mentioned here, such as fixed deposits, mutual funds, stocks, or government schemes, have different levels of risk and returns.

Returns from investments can change depending on market conditions, interest rates, and economic factors. Past performance does not guarantee future results. Before investing, you should check your financial goals, risk tolerance, and investment time horizon, and consider consulting a qualified financial advisor if needed.

Conclusion

In 2026, investors have more choices than ever.

Some people prefer safety. Others prefer growth. Most need a balance.

From my experience, the best investment options in India are not about chasing the highest returns. They are about choosing what fits your life, goals, and comfort level.

Start early. Stay consistent. Be patient.

That’s what really builds wealth.

The best investment decision is simply starting today.

You can also read this

Complete Share Market Guide for Beginners: How to Invest