By Rupesh Kumar

Published: November 21, 2025

Last Updated: March 02, 2026

Introduction

When I got my first proper salary, I felt very confident. I thought as long as money is coming every month, everything is safe. But one sudden medical emergency in my family changed my thinking completely. Within a few days, most of my savings were gone. I noticed how stressful it feels when you don’t have backup money. That problem happened to me, and I never want anyone to face that pressure.

That is why learning how to build an emergency fund is not just financial advice — it is real life protection. In India, one job loss, one hospital bill, or one family emergency can disturb your full budget. An emergency fund gives mental peace. It gives you control. In this guide, I will share practical steps from my own experience on how to create emergency fund properly and safely.

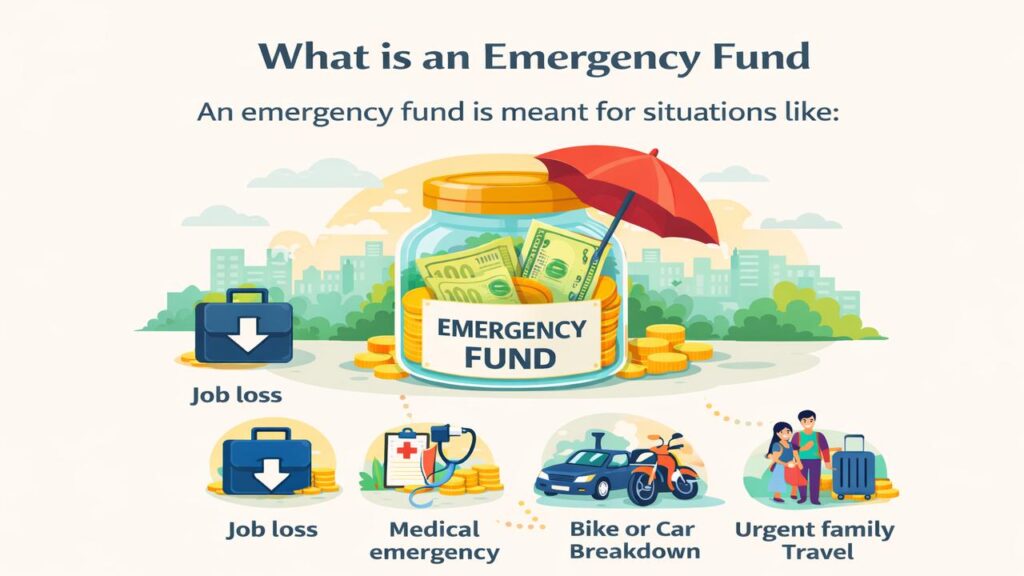

What is an Emergency Fund

An emergency fund is money kept separately only for unexpected and serious situations in life. It is your financial backup when something goes wrong without warning.

An emergency fund is meant for situations like:

- Job loss

- Medical emergency

- Sudden house repair

- Bike or car breakdown

- Urgent family travel

- Business slowdown or delayed payments

These are real problems. These are situations where income may stop but expenses continue.

It is not for:

- Mobile upgrade

- Vacation

- Festival shopping

- EMI for a luxury item

- Impulse online purchases

In simple words, an emergency fund is the money that gives you breathing space when life becomes uncertain. It helps you stay calm, avoid loans, and protect your family’s financial stability.

Emergency Fund Rule

The emergency fund rule is simple and practical — save at least 3 to 6 months of your essential monthly expenses.

Earlier, I used to think keeping so much money aside is unnecessary. But when one month my freelance payment got delayed, I noticed how stressful it feels when income stops but expenses continue. That situation taught me this rule is not optional — it is protection.

First, calculate only your essential expenses, not luxury spending.

Example:

| Monthly Essential Expense | Amount |

|---|---|

| Rent | ₹12,000 |

| Groceries | ₹6,000 |

| Electricity & Bills | ₹2,000 |

| EMI | ₹5,000 |

| Total | ₹25,000 |

Now apply the rule:

- 3 months = ₹75,000

- 6 months = ₹1,50,000

If you have a stable job, 3–6 months is usually enough.

If your income is unstable (business or freelancing), 6–9 months is safer.

I personally keep more than 6 months because I have seen how unpredictable income can be. This rule gives peace of mind. It gives you time to handle problems calmly without borrowing money.

How to Build an Emergency Fund Fast: 7 Simple Steps

When I first decided to build my emergency fund, I thought it would take years. But once I followed a clear plan, I noticed progress much faster than expected. If you are serious about learning how to build an emergency fund fast, these practical steps will help you.

This is exactly how I did it.

1. Calculate Your Real Survival Expenses

First, understand how much you actually need every month to survive.

Do not include eating out, shopping, or subscriptions. Only include:

- Rent

- Groceries

- Basic bills

- EMI

- School fees

When I calculated honestly, I realised my actual survival expense was much lower than my full spending. This made the emergency fund target more achievable.

2. Fix a Clear Target Amount

The basic emergency fund rule says 3–6 months of essential expenses.

If your monthly expense is ₹30,000:

- 3 months = ₹90,000

- 6 months = ₹1,80,000

Write this number clearly. When I wrote my target on paper, saving became more focused. Without a number, there is no direction.

3. Open a Separate Account

One mistake I made earlier was keeping savings in the same account. Slowly, it got spent.

So I opened a separate savings account only for emergency money. This small step made a big difference. If you really want to understand how to create emergency fund properly, separation is very important.

Out of sight means out of spending.

4. Automate on Salary Day

If you want to build your emergency fund seriously, automate it. I learned this after many months of failed saving attempts. I used to save at month end, but expenses always increased. I noticed money disappears when it sits in the main account. Now, I transfer a fixed amount on salary day itself. Saving first, spending later — this simple rule made my emergency fund grow steadily without stress.

5. Cut 2–3 Unnecessary Expenses Temporarily

If you want to know how to make an emergency fund fast, short-term sacrifice helps.

For 6–8 months:

- Reduce food delivery

- Avoid gadget upgrades

- Reduce impulse purchases

- Pause unnecessary subscriptions

I did this for one year. It was not permanent. But it helped me reach my target quickly.

6. Use Extra Income Smartly

Whenever you receive:

- Bonus

- Freelance income

- Incentive

- Gift money

Put at least 50% into your emergency fund.

I noticed that lump sum amounts speed up progress more than small monthly savings.

7. Increase Savings Gradually

When I started building my emergency fund, I could not save a big amount. So I began with a small fixed sum. It felt manageable and did not disturb my monthly budget. After a few months, whenever my salary increased or expenses reduced, I increased my savings amount slightly.

I noticed that small increases like ₹500 or ₹1,000 make a big difference over time. You don’t need to save a huge amount from day one. Start small, stay consistent, and increase slowly. This method builds your emergency fund steadily without financial pressure.

When Should You Stop Adding ?

Once you reach:

- 6 months of expenses (stable job)

- 9–12 months (unstable income)

After that:

Start investing extra money in:

- SIP

- PPF

- NPS

- Index funds

But review emergency fund yearly.

If expenses increase, increase fund size.

Emergency Fund vs Savings vs Investments

When I started earning, I used to think all money in my bank account is the same. Later I noticed that emergency fund, savings, and investments have completely different purposes. Once I separated them, my financial planning became much clearer.

- Emergency Fund → Used only for unexpected situations like job loss, medical emergency, or urgent repairs

- Savings → Used for short-term planned goals

- Investments → Used for long-term wealth creation

Each serves a different purpose. Don’t mix them.

Common Mistakes to Avoid

When I was learning how to build an emergency fund, I made a few mistakes that slowed my progress. I noticed many people repeat the same errors.

- Keeping emergency money in the same account as daily spending

- Investing emergency fund in stocks for higher returns

- Using it for shopping or vacations

- Not following the basic emergency fund rule

- Not increasing the fund when expenses grow

Avoiding these simple mistakes makes your emergency fund strong and reliable when you actually need it.

The Week That Changed My Money Habits

A few years ago, my father suddenly fell sick and we had to admit him to the hospital. Tests, medicines, and advance payment had to be done immediately. I had some savings, but not enough for everything. I noticed how stressful it feels when you are standing at a hospital counter and checking your bank balance again and again. That problem happened to me, and I had to borrow a small amount from a friend.

That week changed my mindset completely. I understood that earning money is not enough. After that, I seriously focused on how to build an emergency fund and started saving every month without fail. Today, because of that experience, I feel much more secure and confident during unexpected situations.

Limitations & Disclaimer

This guide on how to build an emergency fund is based on my personal experience and general financial knowledge. It is for educational purposes only. Every person’s income, responsibilities, and risk level are different. What worked for me may not be perfect for you. Always review your own situation carefully and consult a qualified financial advisor before making major financial decisions.

❓ FAQs about how to Build an Emergency Fund

1. How much emergency fund should I have?

Follow the basic emergency fund rule — save 3 to 6 months of essential expenses. If your income is unstable, keep 6 to 9 months. I personally prefer more than 6 months because income is never 100% guaranteed.

2. Can I start building an emergency fund with low income?

Yes, absolutely. I started small. Even ₹1,000–₹2,000 per month works. The key is consistency. Increase slowly whenever income increases.

3. Should I build emergency fund before investing?

Yes. First protection, then growth. I made the mistake of investing early without proper backup. When an urgent expense came, I had to withdraw investments.

4. Can I use credit card instead of emergency fund?

Credit card is not emergency money. It is borrowed money with interest. Emergency fund means your own money without debt stress.

5. How long does it take to build an emergency fund?

It depends on your income and saving rate. When I started, it took me almost 18 months to complete 6 months of expenses. If you save aggressively and use bonuses wisely, you can build emergency fund faster.

Conclusion

When I didn’t have an emergency fund, every unexpected expense felt like a crisis. I noticed that without backup money, even small problems create stress. This problem happened to me once, and it changed my mindset completely. After learning how to build emergency fund and following the emergency fund rule, I felt real financial confidence. Start small, stay consistent, and protect your future first.

If you want to explore more practical strategies on building a sustainable emergency fund, you can also read this detailed guide by RBL Bank which explains the concept clearly with real-world examples.

You can also read this :-

Best Investment Options in India 2026 | Safe & High Returns