By Rupesh Kumar

Published: November 16, 2025

Last Updated: February 24, 2026

Introduction

When I first opened my bank account, I only had a debit card. I thought credit card and debit card were almost the same. This problem happened to me because no one clearly explained the difference between credit card and debit card. I noticed many people around me were also confused.

Later, when I applied for my first credit card, I understood that both cards work very differently. In this blog, I will explain credit card vs debit card in simple language, with real experience, so you can decide which is better for you.

First, Let’s Understand the Basic Difference

The difference between credit card and debit card is very simple:

- Debit card = Your own money

- Credit card = Bank’s money (you repay later)

When I use my debit card, money is deducted immediately from my bank account. There is no tension of a bill later.

But when I use my credit card, I am basically borrowing money for 30–45 days. If I pay on time, no interest. If I forget, heavy charges.

This small difference changes your financial habits completely.

My Real Experience with Debit Card

In my early job days, I preferred debit card. I noticed it helped me control spending. If my account had ₹5,000, I could not spend ₹10,000. Simple.

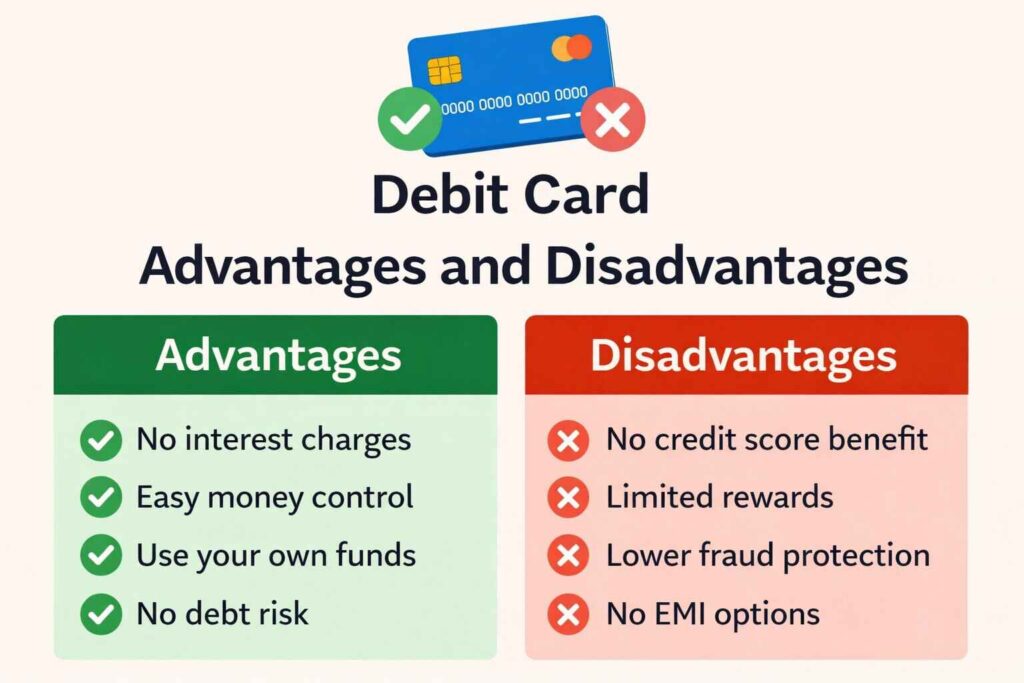

Debit Card Advantages and Disadvantages

Debit Card Advantages

- No interest charges tension

- No bill at month end

- Easy to use

- Direct payment from account

- Good for beginners

- No risk of debt

Debit Card Disadvantages

- No credit score building

- Very Limited rewards

- Daily transaction limits

- Less protection in some fraud cases

- No EMI benefits in many cases

Once, I wanted to book a flight ticket on EMI using debit card, but option was not available. That’s when I felt its limitation.

My Real Experience with Credit Card

When I got my first credit card, I was excited because of cashback offers and reward points. I noticed I was getting benefits on online shopping.

But I also learned an important lesson.

One month, I forgot to pay the full bill. This problem happened to me because I ignored the due date. The bank charged interest and late fees. That’s when I understood that credit cards require discipline.

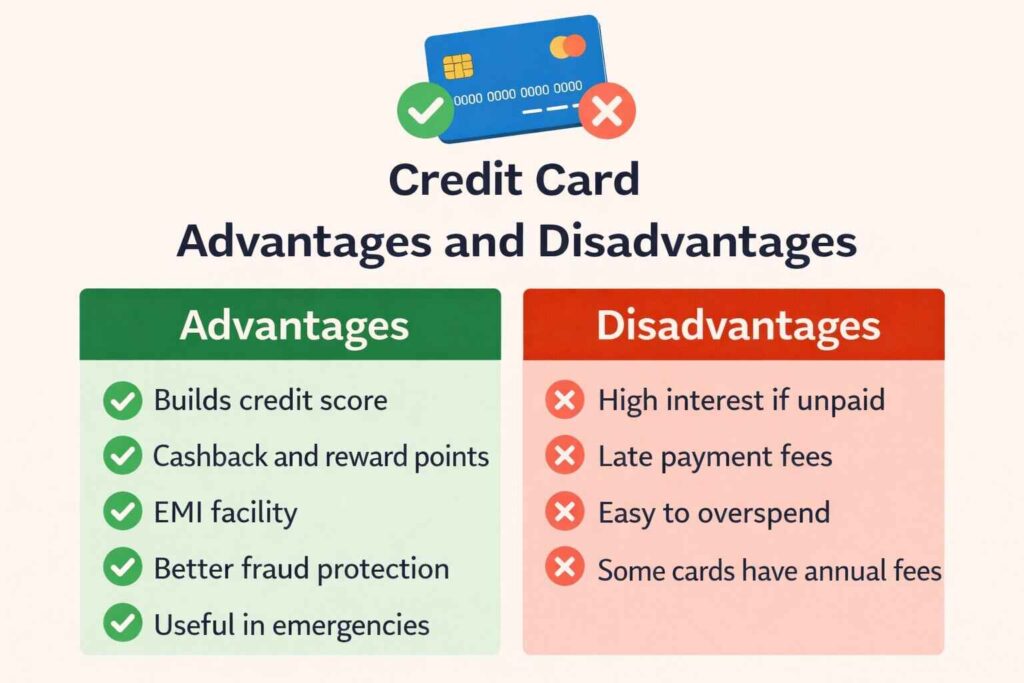

Credit Card Advantages and Disadvantages

Advantages

- Builds credit score

- Cashback and reward points

- EMI facility

- Better fraud protection

- Useful in emergencies

Disadvantages

- High interest if unpaid

- Late payment charges

- Can lead to overspending

- Annual fees (in some cards)

If you are responsible with payments, credit card can be very powerful. But if you spend without planning, it can become stressful.

Credit Card vs Debit Card: Simple Comparison Table

Here are the most important differences:

| Feature | Credit Card | Debit Card |

|---|---|---|

| Money Source | Borrowed money (bank pays first) | Your bank balance |

| Interest | Yes (if unpaid after due date) | No |

| Credit Score Impact | Yes, builds credit score | No impact |

| Spending Limit | Fixed credit limit | Available account balance |

| Rewards | Usually available (cashback, points) | Limited rewards |

| Risk of Debt | High (if misused) | Low |

| Security / Fraud Protection | Strong protection, easier chargeback | Moderate protection |

| International Usage | Widely accepted, useful for travel | Accepted, but may have limits |

| Minimum Balance Requirement | No bank balance needed | Bank may require minimum balance |

| Lounge Access (Premium Cards) | Available on selected cards | Rare (only select premium debit cards) |

My Honest Advice:

In the debate of credit card vs debit card, there is no universal winner.

Debit card gives safety.

Credit card gives benefits.

The real winner is your financial discipline.

If you are responsible, credit card can help you grow your credit score and enjoy rewards. If you struggle with spending control, stick with debit card.

One Important Mistake People Make

Many people think credit card means “extra money.” I also thought like this once. That mindset is dangerous.

Credit limit is not your income. It is temporary borrowing.

Once I started treating my credit card like a debit card — meaning I only spent what I could repay — my financial stress reduced completely.

That experience taught me one simple rule:

Credit limit is not your income.

Now I use my credit card only when I am sure I can repay the full amount without stress. That small change made a big difference in my financial peace.

Real Personal Example

A few years ago, my monthly salary was around ₹30,000–₹33,000. At that time, my credit card limit was ₹90,000. Seeing that high limit made me feel comfortable.

I bought a smartphone worth ₹42,000 using my credit card. I thought I would easily manage it next month. My card’s interest rate was around 36% per year (about 3% per month).

But that month, some unexpected home expenses came. I could not pay the full bill and only paid the minimum due. I noticed next month extra interest was added. This problem happened to me because I did not understand how costly minimum payment can be.

That’s when I understood one important lesson — always try to pay the full credit card bill. Minimum due is not a smart option, it is only for emergency situations.

Limitations & Disclaimer

This content is only for general information about credit card vs debit card. It is not financial advice. The right choice depends on your income, spending habits, and bank rules. Features and charges may be different for each bank.

Before using any card, check fees, interest rates, and terms with your bank. We are not responsible for any loss, extra charges, or misuse. Always use cards carefully and spend within your limit.

Frequently Asked Questions

1. What happens if I don’t pay my credit card bill?

If you don’t pay, bank charges interest and late fees. Your credit score also drops. I noticed even one late payment can affect your score for months.

2. Is credit card risky ?

Credit card is risky only if you miss payments. This problem happened to me once when I forgot the due date and had to pay extra charges. If you always pay the full amount on time, it is very safe and useful.

3. Does a debit card build credit score ?

No, debit cards do not build credit score. I learned this later. Only credit cards and loans help in building your credit history, if you pay on time.

4. Should I keep both cards ?

Yes, having both is practical. I use debit card for ATM withdrawals and daily spending. I use credit card for online shopping and travel bookings. Both serve different purposes.

5. Can students get credit cards?

Some banks offer student-friendly credit cards or add-on cards with low limits.

Conclusion

After using both cards for years, I honestly believe the debate of credit card vs debit card is not about which card is powerful — it is about how responsible you are. I noticed when I used my debit card, my spending stayed under control. But when I understood the difference between credit card and debit card, I realized credit cards can offer bigger benefits if handled wisely.

If you are still thinking about which is better credit card or debit card, ask yourself how disciplined you are with money. Credit card advantages and disadvantages both exist, just like debit card advantages and disadvantages. The right choice depends on your income, spending habits, and financial goals.

In simple words, debit card gives safety, and credit card gives opportunities. Choose smartly, spend carefully, and always stay financially aware.

HDFC Bank resource: “Difference Between Credit Card vs Debit Card” — Detailed comparison covering benefits, interest rates, fees, and practical usage.